Why I Think AMD is UNDERVALUED - Analyzing AMD's Financials, Growth, and Market Position

Why AMD doesn't need to be beat Nvidia to be a primary GPU distributor

Abhishek Jolad

7/23/20246 min read

Overview of the Business (Form 10k)

AMD is a global semiconductor powerhouse, driving innovation in the data center, gaming, and embedded markets. Their diverse portfolio includes cutting-edge CPUs, GPUs, DPUs, FPGAs, AI accelerators, and Adaptive SoCs. As leaders in adaptive computing, AMD's solutions are transforming industries from healthcare to automotive, industrial to storage and networking.

The company's strategic focus extends beyond traditional computing, strongly emphasizing AI development and training. Recent acquisitions have bolstered AMD's AI software capabilities, positioning them to challenge industry leader Nvidia in this rapidly growing sector

Financial Overview

AMD’s business is structured into 4 segments:

Data Center: Developing high-performance computing products for data centers, competing directly with Nvidia.

Client: Producing CPUs and GPUs for PCs and desktops, rivaling Intel in this space.

Gaming: Creating discrete GPUs and semi-custom SoC products for the gaming industry.

Embedded: Integrating adaptive computing products into various applications, competing with Intel in this segment.

Competition

AMD faces intense competition, especially from Nvidia and Intel and even on-the-rise semiconductor companies such as Qualcomm and Broadcom. According to their 10-K filings, there are a few main factors that determine their competitiveness amongst others:

Timely product introductions, product quality, features, and capabilities, energy efficiency, reliability, processor performance, form factor, price, cost-effectiveness, and software and hardware compatibility

Research & Development

AMD's Research and Advanced Development (RAD) division is at the forefront of the company's innovation efforts, driving transformative technologies that expand business opportunities and enhance existing product lines. The RAD team focuses on several key areas:

High-Performance Computing (HPC): Pushing the boundaries of performance scaling across all AMD products, from data center CPUs and GPUs to high-end desktops and gaming consoles.

Advanced Memory Systems: Pioneering new directions in memory technologies to overcome the "Memory Wall" and improve system responsiveness.

Machine Learning (ML): Developing solutions to make AMD the preferred platform for ML applications across various computing environments.

Energy Efficiency: Improving power efficiency across AMD's entire range of SoCs, from data centers to mobile devices.

Software Optimization: Creating software solutions that boost hardware utility, reduce power consumption, and streamline user tasks.

Qualitative Analysis

SWOT Analysis

Strengths

Diverse Product Range: AMD offers a broad spectrum of hardware components, including CPUs, GPUs, FPGAs, and accelerators, catering to various industries such as gaming and AI.

Strong Leadership: Under Dr. Lisa Su's leadership, AMD has transformed from struggling to one of the top performers in the S&P 500, successfully competing with giants like Intel and Nvidia.

Strategic Partnerships: AMD has established significant partnerships with major tech companies like Oracle, Microsoft, and Sony, supplying them with GPUs.

Weaknesses

Reliance on TSMC: AMD heavily depends on TSMC for chip manufacturing, making it vulnerable to chip shortages and production delays.

Intense Competition: AMD faces fierce competition from Nvidia, the leading GPU producer in the AI sector, adding pressure to maintain high performance.

Opportunities

AI and Machine Learning: The growing demand for AI models necessitates powerful GPUs for training on complex data, presenting a significant opportunity for AMD.

Mobile Market Expansion: AMD has the potential to develop smartphone chips to compete with Apple and Qualcomm, though this requires substantial investment.

Threats

Supply Chain Disruptions: Dependence on TSMC could lead to significant slowdowns if there are disruptions, impacting AMD's competitive position against Nvidia and Intel.

Government Regulations: Trade regulations, such as restrictions on AI product exports to China, could severely impact AMD’s sales, as seen with Nvidia's stock performance.

Fundamental Analysis

Income Statement

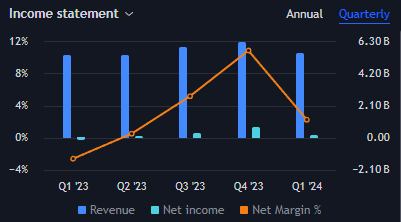

Revenue and Net Income

Revenue is consistent with slight increases over the quarters.

Net income showed fast growth but quickly slowed down drastically during Q1 2024.

R&D Spending

R&D spending nearly doubled from 2021 to 2022 but stayed almost the same from 2023 to 2024.

Sales Costs

Sales costs stayed almost the same with only a slight drop from the previous fiscal year.

Balance Sheet

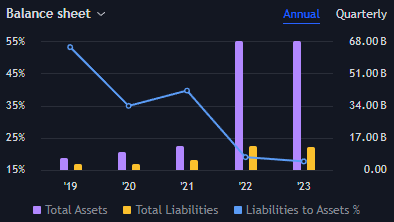

Total Assets

Total assets stayed nearly the same when compared to the previous fiscal year

Looking at the previous years, we can see that there is massive growth in their total assets.

Total Liabilities

Total Liabilities also stayed nearly the same but there was slight growth when compared to the previous years.

Return on Assets (ROA)

AMD’s ROA is 1.65% which isn’t preferred from an investing perspective

Return on Equity (ROE)

ROE is relatively higher than ROA, suggesting possible excess debt.

Price to Book (P/B)

AMD’s P/B ratio is 4.48 which is less than the industry average of 7.38

This indicates that it may be undervalued compared to its peers, especially Nvidia, whose P/B ratio is 61.82

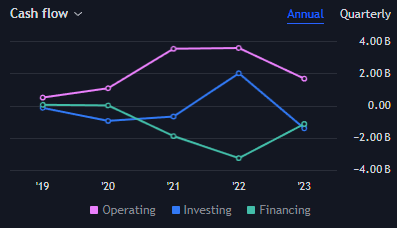

Cash Flow Statement

Operating Activities

Net cash from operating activities decreased by 53%, signaling that AMD is struggling to generate cash from their core business activities

Investing Activities

Net cash provided by investing activities decreased drastically by 171%. This could be due to AMD increasing their investment expenditures

Cash and Cash Equivalents

AMD’s cash and cash equivalents decreased at the end of the year by 18% which indicates that they might be increasing their spending

Financial Ratios

Valuation (Price):

Price-to-Earnings (P/E) Ratio:

227.30

Interpretation: As the industry average for the P/E ratio is 50.38, a P/E ratio of 227.3 may indicate that AMD is quite overvalued.

Profitability:

Return on Equity (ROE):

2.01%

Interpretation: This shows a low level of profitability for AMD which is likely due to intense competition from Nvidia and Intel

Liquidity:

Current Ratio:

2.64

Interpretation: This signifies that AMD is well-positioned to cover any short-term debts and is in a good financial situation in terms of liquidity

Debt (Solvency):

Debt-to-Equity Ratio:

0.05

Interpretation: AMD has greater financial flexibility and can even take on more debt to increase shareholder returns.

Asset Turnover Ratio:

0.08

Interpretation: This implies that AMD is not effectively leveraging its assets to generate profit especially since the industry average is between 0.52 and 0.63. This further shows that AMD is less effective in utilizing their assets compared to their competitive peers like Nvidia.

Relative Evaluation Using a DCF Model

AMD’s intrinsic value is estimated to be $200 (worst case) to $260 (best case)

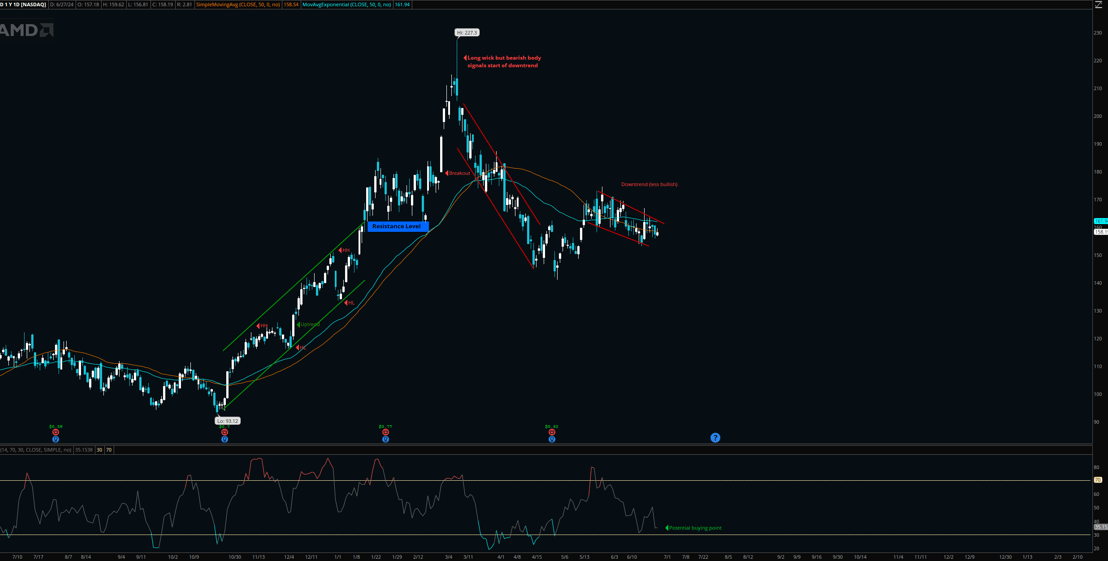

Technical Analysis

From the start of November 2023, AMD has been in a strong uptrend, consistently making HHs and HLs

During mid-January, the stock was in a consolidation period (sideways market) but maintained a resistance level of $162

Breakout occurred at the start of March, leading to an all-time high of $227 a couple of days later.

However, the long wick but bearish body signaled the start of the downtrend which continued until their most recent quarterly report (4/30)

The price rose for some time but returned to another (less bearish) downtrend.

Based on the low RSI level, the 157-160 price level could be a safe buying point

Summary

AMD faces intense competition, particularly from Nvidia in the AI GPU market and Intel in the CPU market. However, AMD's strong balance sheet, low debt, and focus on high-growth areas like AI and data center solutions position it well for future growth. Challenges include the need to improve asset utilization efficiency and potentially increase profitability relative to equity. The company's heavy reliance on TSMC for manufacturing also presents a potential risk.

While Nvidia currently dominates the AI chip market with an estimated 80-90% market share, AMD is positioning itself as a strong alternative. AMD's strategy of offering more cost-effective solutions, such as its upcoming MI300 series chips, could potentially capture market share, especially if Nvidia struggles to meet the high demand for its expensive AI GPUs. AMD's recent introduction of new AI-optimized processors for PCs also demonstrates its commitment to competing in the expanding AI market.

Overall, AMD appears to be in a strong financial position with significant growth opportunities, particularly in the AI and data center markets. However, the company still faces stiff competition and efficiency challenges. AMD's success will likely depend on its ability to execute its AI strategy effectively and capitalize on any supply constraints faced by its competitors.